All insurance companies have an internal complaints process, which you must follow to obtain a Final Position Letter from your insurer before you bring your complaint to us at the OmbudService for Life and Health Insurance (OLHI).

Once you have received a Final Position Letter, you can submit your complaint to us.

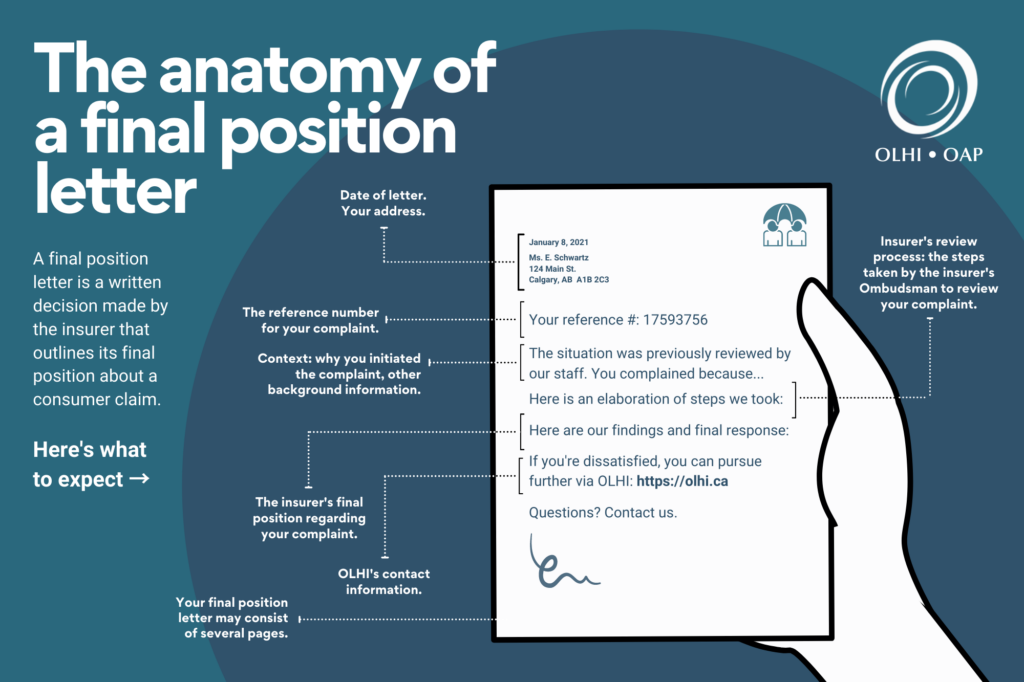

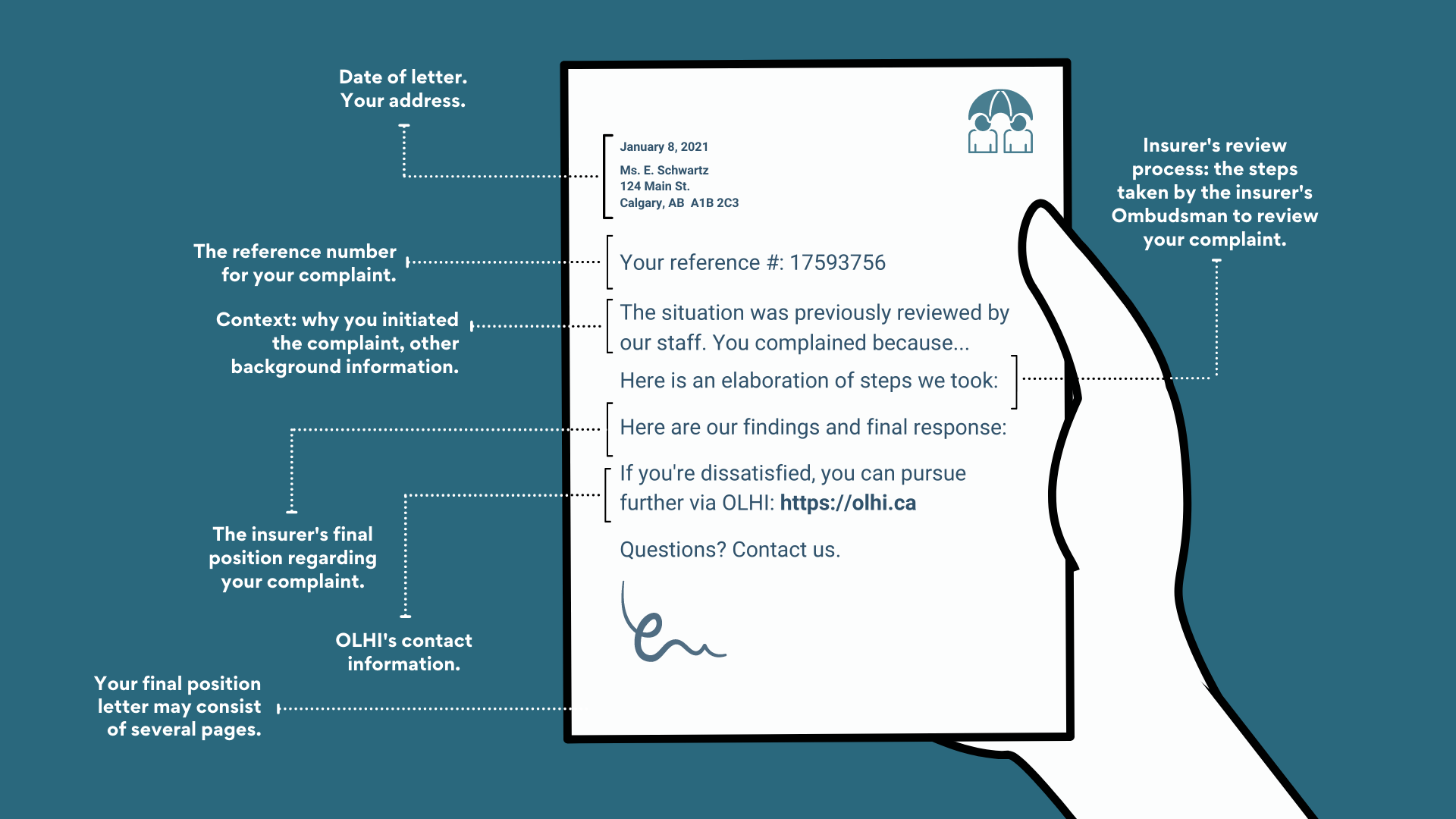

Got your Final Position Letter? Here’s the next step:

Once you have received a Final Position Letter from your life or health insurance provider, you can submit a complaint to our ombudservice.

If your complaint is reviewable and has merit, we can provide another impartial review of your insurer’s final position on a health or life insurance claim.

Take a few minutes to learn more about our complaints process so you know what to expect:

Did you know that you can make a complaint if your life or health insurance company denies your claim?

Before you submit your complaint to us at the OmbudService for Life and Health Insurance (OLHI), you first need to go through your insurance company’s internal complaint process.

Can I go directly to OLHI with my denied insurance claim?

OLHI can’t review a complaint about a denied claim if you haven’t gone through your insurer’s internal process.

We’ll know that you completed this process if you have a “final position letter”—it’s one of the first things we’ll ask for after you submit a complaint to OLHI.

How to submit a complaint to your life or health insurance company

1. Appeal your denied claim.

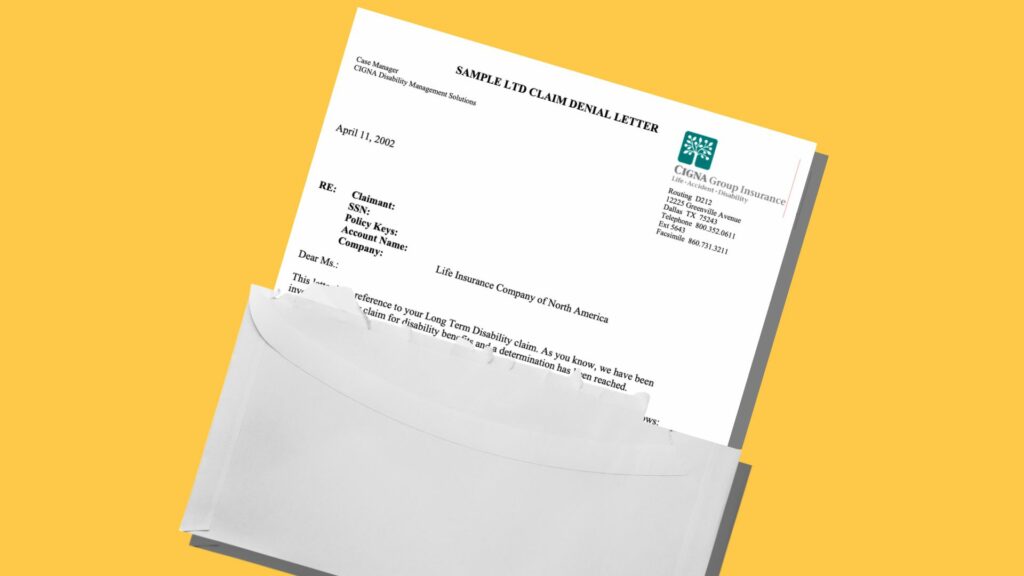

If your life or health insurance claim gets denied, a Case Manager will send you a claim denial letter. Each submitted claim gets assigned to a Case Manager, whose job is to review these claims to see if they are payable—or not.

A claim denial letter will provide step-by-step instructions on how to appeal your denied claim.

A claim denial letter will provide step-by-step instructions on how to appeal your denied claim. You’ll likely need to provide additional details (in writing) to your insurer to clarify the context of your claim.

If you receive a second claim denial letter, now you have the grounds to file a complaint.

Tip: Be calm and polite.

Trying to resolve a complaint can be frustrating and stressful. Our experience is that a courteous manner leads to an easier and faster resolution.

2. Submit your life or health insurance complaint to a Complaint Officer.

Once you’ve unsuccessfully appealed your denied claim, you can escalate your situation to a Complaint Officer at your insurance company.

A Complaint Officer has the authority to make a final decision about your complaint.

Before sending your complaint, contact your insurance company to determine to whom you should address your complaint and what documentation you need to attach.

Tip: Submit your complaint in writing.

It’s usually best to send your complaint in writing. Many insurance companies will have an email address or online form you can use to make your complaint. You may also be able to send it by mail.

Before sending your complaint, contact your insurance company to determine to whom you should address your complaint and what documentation you need to attach.

OLHI has a Consumer Complaint Officer Listing tool that allows you to quickly find the contact information for your insurance company’s Complaints Officer. (If you don’t see your insurance company on this list, it means they aren’t a member company of OLHI.)

Tip: How to format your written insurance complaint

• Put “Complaint” at the top of your letter or in the subject of your email.

• Be clear about what went wrong and when.

• Tell your insurance company what you expect as a solution.

3. Submit your life or health insurance complaint to a Complaint Officer.

Once you complete your insurance company’s complaint process, you will receive a “final position letter.” If you don’t receive a final position letter, ask for one from the Complaint Officer.

If you don’t receive a final position letter, ask for one from the Complaint Officer.

4. Contact OLHI if you haven’t heard from your Complaint Officer in 90 days or more.

If your insurer takes longer than 90 days to reach a decision, ask OLHI to contact your company to inquire about the status of your complaint.

What to do if you’re unhappy with your insurer’s final decision on your complaint

Followed all the steps above, but you’re still dissatisfied with your insurer’s final position? You can now submit a complaint to OLHI. If your case is reviewable and has merit, we can provide a free, independent, and impartial review.

Thirty years ago, Mrs. B. purchased life insurance. The premium would change over the years and the cash surrender value would be flexible but, as she understood it, she was guaranteed a paid-up $200,000 policy at age 65. This original policy was subsequently transferred to several insurers over the years.

When she turned 65, Mrs. B. received a letter informing her that her policy was now paid up; no more premiums were necessary to maintain the value of $200,000 and to keep her policy in force. Mrs. B. stopped making payments but, several years later, received a letter advising that her policy was now valued at $158,000.

Although no further premiums were required to keep the policy in force, the insurer stated that the sum insured continued to be reviewed for adjustment. Mrs. B. disagreed and contacted OLHI for a free, independent and impartial review of her file. She provided us with the final position letter and copies of all her correspondence with the various insurers that had owned the policy over the years. We also received the current insurer’s file.

OLHI’s first impression was that there would likely be no grounds to negotiate as the decrease in the sum insured was likely contractual.

However, OLHI’s Dispute Resolution Officer (DRO) discovered that Mrs. B. had a letter from the original insurer, guaranteeing in writing the sum insured of $200,000, with no adjustments to that sum. For this reason, the complaint was escalated to an OmbudService Officer (OSO) for further investigation.

Speaking with the insurer, the OSO concurred that the policy clearly outlines the recalculations of the premiums and the fact that the sum could change after age 65. However, he also noted that the guarantee letter could not be overlooked. The insurer, after additional review, agreed to honour the commitment that the previous insurer had made, confirming that the sum insured would not be recalculated in future.

Disclaimer: Names, places and facts have been modified in order to protect the privacy of the parties involved. This case study is for illustration purposes only. Each complaint OLHI reviews contains different facts and contract wording may vary. As a result, the application of the principles expressed here may lead to different results in different cases.

Mr. Y. had been receiving long term disability (LTD) benefits from his insurer for two years. He applied for and was accepted by Canada Pension Plan (CPP) for disability benefits. Since Mr. Y. had received retroactive amounts from CPP, the insurer followed up with a request for the overpayments they had made to him.

At question was whether the calculations were accurate. Mr. Y. disputed the insurer’s calculations and, after receiving a final position letter, called OLHI for help.

OLHI’s Dispute Resolution Officer (DRO) reviewed the consumer’s documents and the insurer’s file. She read the policy contract section on coordination of benefits, which refers to a combination of benefits coverage from more than one extended health plan. The DRO also reviewed how the insurer applied the indexations, which are adjustments to income payments to protect against inflation. She agreed with the consumer’s claim that the insurer may have erred in applying the indexations. She recommended that the complaint be escalated to an OmbudService Officer (OSO) for further investigation.

The OSO confirmed with Mr. Y. that he was receiving his LTD and CPP benefits, and that he had repaid to the insurer the overpayment requested. The issue remaining was if and how indexation should be applied in the re-calculation of his LTD benefits.

The OSO wrote to the insurer, suggesting that their business unit had focused on the correctness of the calculation but not on the correctness of the overall formula. The OSO also suggested that it might be helpful if the interpretation of the policy contract could be reviewed by the insurer’s legal department.

The insurer’s counsel reviewed both the OSO’s recommendation and the policy contract wording. Although they identified additional areas in the contract that would affect the calculation of the benefit in their favour, they agreed that the section on coordination of benefits supported Mr. Y.’s position. In good faith, the insurer proposed a compromise, which was accepted by the consumer.

Disclaimer: Names, places and facts have been modified in order to protect the privacy of the parties involved. This case study is for illustration purposes only. Each complaint OLHI reviews contains different facts and contract wording may vary. As a result, the application of the principles expressed here may lead to different results in different cases.

By continuing your navigation on this site, you accept the use of cookies.

These are designed to improve your user experience on our site by collecting traffic statistics and information on your behaviour.